Price:$27.00

STR Quit Date Calculator – Airbnb Income Replacement Spreadsheet (Excel)

Here's what's eligible:

- Your order doesn't match the item description or photos

- Your item arrived damaged

- Your item arrived after the estimated arrival window

- Your item didn't arrive or was lost in the mail

You can only make an offer when buying a single item

Highlights

Run your rentals before they run you. A career-transition planner for STR hosts asking the real question: when can I quit? Calculates your quit date — optimistic and conservative — based on your portfolio's actual numbers. Excel.

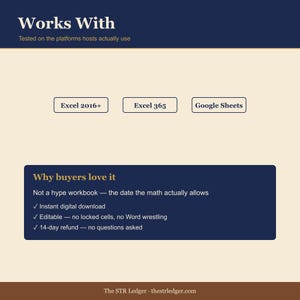

This is not a hype workbook. It will not tell you to quit tomorrow. It will tell you, based on your W2, your portfolio's current Schedule E numbers, your savings rate, and your household expenses, how many years and months until the math actually works. The answer is rarely what you hoped. It is usually further out than the gurus claim and closer than you fear. The spread between optimistic and conservative is the conversation you have been avoiding with your partner.

═══════════════════════════════════════════

WHAT'S INCLUDED — LITE ($27 ETSY)

═══════════════════════════════════════════

Excel workbook (3 tabs):

- Start — THE quit date. Optimistic and conservative dates side by side. The spread between them. Four critical numbers: properties needed, cash needed at quit, healthcare bridge cost, projected Y1-after-quit net.

- Current State — W2 income, STR portfolio (gross + Schedule E line 26 net), household expenses, liquid runway, partner W2, employer benefits value (401k match, health insurance, life, disability).

- Target State — replacement income, buffer multiple (default 1.5×), reserve target, properties needed at current per-property economics.

Lite calculates years-to-quit. Full adds the acquisition schedule, healthcare bridge math, partner risk-share, and the printable Conversation Doc.

═══════════════════════════════════════════

WHAT'S INCLUDED — FULL ($47 OWN-SITE)

═══════════════════════════════════════════

All 3 Lite tabs, plus:

- Acquisition Schedule — year-by-year property adds with cash deployment. Y1 net per added property defaults to 65 percent of stabilized (because Year 1 is harder than the brochure).

- Risk Plan — healthcare bridge math (COBRA at 102 percent of premium for 18 months, then ACA), insurance gap, partner risk-share slider 1 to 5 driving the conservative scenario.

- Quit Date Calculator — toggle Optimistic vs Conservative. Different occupancy assumptions, different acquisition pace, different appreciation, different buffer multiples.

- Conversation Doc — one-page printable for the kitchen table conversation. Quit dates, four critical numbers, three biggest swing factors, action plan, partner sign-off lines.

═══════════════════════════════════════════

WHY THIS PAYS FOR ITSELF

═══════════════════════════════════════════

The cost of an extra year at a job you want to leave is not measured in dollars. It is measured in mornings. But the cost of quitting too early — running out of runway before stabilization, taking a 401k loan to cover a roof repair, going back to W2 at 50 percent of your prior salary — that has a number, and the number is large.

Most "when can I quit" math is napkin math. This workbook runs the spreadsheet version. Healthcare bridge alone — 18 months of COBRA at $14,400/yr family of 4 plus 6 months of ACA — is roughly $28,800. Most planners forget this entirely. We do not.

═══════════════════════════════════════════

WHO IT'S FOR

═══════════════════════════════════════════

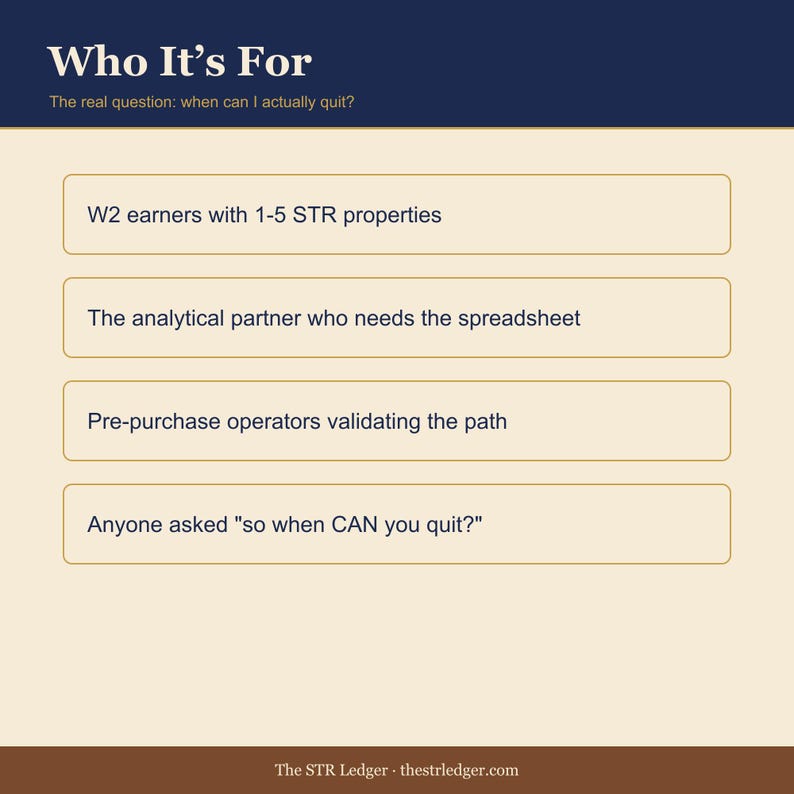

- W2 earners with 1 to 5 STR properties asking when they can quit

- The analytical partner who needs the spreadsheet to confirm or kill the dream

- Pre-purchase operators validating that the path is actually realistic before buying

- Anyone whose partner has asked "so when CAN you quit?" and they did not have an answer

═══════════════════════════════════════════

WHO IT'S NOT FOR

═══════════════════════════════════════════

- Anyone looking for a "quit your job in 90 days" hype workbook. We do not sell that.

- Households relying on W2 spousal income that has not been factored in. The workbook handles dual-W2 cleanly; single-income paths work but are not deeply modeled.

- International hosts. US healthcare and tax assumptions only.

═══════════════════════════════════════════

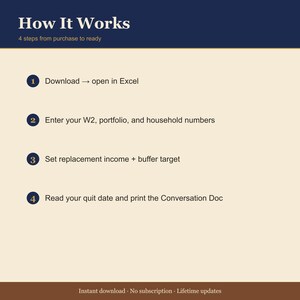

HOW IT WORKS

═══════════════════════════════════════════

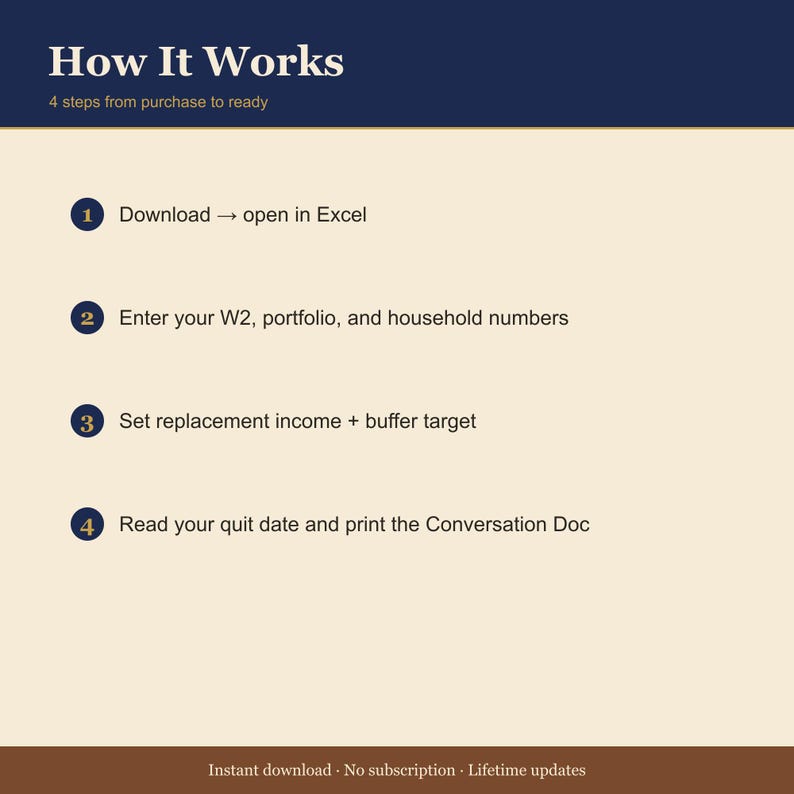

1. Purchase, instant download.

2. Open Current State — fill in W2 net, current STR portfolio numbers (use last year's Schedule E line 26), household expenses, partner W2 if applicable.

3. Open Target State — set replacement income target (default = current W2 net + benefits cost), buffer multiple, reserve target.

4. Open Start — read the optimistic and conservative quit dates. Read the spread.

5. Full only: open Acquisition Schedule. See year-by-year property adds with cash deployment.

6. Full only: open Risk Plan. Adjust the partner risk-share slider. Watch the conservative date move.

7. Full only: print the Conversation Doc. Put it on the kitchen table.

8. Re-run every time you close on a property. The dates update.

═══════════════════════════════════════════

FAQ

═══════════════════════════════════════════

Q: What does Optimistic vs Conservative actually change?...

Instant Download

Your files will be available to download once payment is confirmed. Here's how.

Instant download items don’t accept returns, exchanges or cancellations. Please contact the seller about any problems with your order.

Etsy Purchase Protection

Shop confidently on Etsy knowing if something goes wrong with an order, we've got your back for all eligible purchases —

see program terms

More from this shop

Visit shop-

Digital download

Partnership Distribution Tracker for STR LLCs — Capital Account + K-1 Prep Spreadsheet — Excel + Sheets

$47.00

-

Digital download

Section 179 Planner for Airbnb Hosts — STR Tax Template — Front-Load Depreciation Calculator — Excel

$27.00

-

Digital download

Airbnb Maintenance Log + Vendor CRM — STR Repair Tracker + Plumber HVAC Contact List — Excel + Sheets

$27.00

-

Digital download

PriceLabs Wheelhouse Beyond ROI A/B Test Spreadsheet — Airbnb Dynamic Pricing Tool Decision — Excel

$27.00

Be the first to leave a review

-

Digital download

STR/AIRBNB CALCULATOR

$9.99

-

Digital download

Beginner Airbnb Investor Bundle | Deal Analyzer, Income & Expense Tracker, Investing Roadmap, Airbnb Guide | Short-Term Rental Tools

$99.00

-

Digital download

Short-Term Rental Income Tracker | Single Property STR Spreadsheet | Easy Expense & Profit Management

$9.99

-

Digital download

Short Term Rental (Airbnb) Cashflow Scenario Calculator

$19.00

-

Digital download

Airbnb Template Income and Expense Spreadsheet | Airbnb Host Template | Rental Property Management | Rainbow

Sale Price $8.98

Original Price $17.97

-

Digital download

Airbnb Profit Calculator: Rental Arbitrage Spreadsheet (Digital Download)

$22.00

-

Digital download

Ultimate Airbnb Hosting/STR Investing Bundle | 20+ Templates for Setup, Management, Guest Experience, Deal Analysis & Tax Tracking

$149.00

-

Digital download

Airbnb Template Income & Expense Tracker Google Sheets | Airbnb Host and Rental Property Management Template

Sale Price $8.98

Original Price $17.97

-

Digital download

Airbnb Template Income and Expense Spreadsheet | Airbnb Host Template | Rental Property Management | Dark Mode

Sale Price $8.98

Original Price $17.97

-

Digital download

Airbnb Template Income & Expense Tracker Google Sheets | Airbnb Host and Rental Property Management Template | Dark Mode

Sale Price $8.98

Original Price $17.97

-

Digital download

STR Investor Starter Pack | Airbnb Excel Templates | Portfolio Dashboard, Analyzer, Guest Experience Tracker

$1.99

-

Digital download

Vacation Rental Income Expense Tracker | Airbnb Finance Planner (Digital Download)

Sale Price $4.98

Original Price $12.44

Shoppers with similar taste loved these

-

Digital download

Rental Property Bookkeeping Spreadsheet: 10-Year Summary (Google Sheet)

Sale Price $24.91

Original Price $33.22

-

Digital download

Client Tracker, CRM Dashboard, Google Sheets, Small Business Template, Lead Tracker, Customer Seller Spreadsheet

Sale Price $13.64

Original Price $22.74

-

Digital download

Rental Property Spreadsheet, Multi-Property Income & Expense Tracker, Rental Property Bookkeeping Google Sheets Template, Property Analyzer

Sale Price $21.00

Original Price $28.00

-

Digital download

Rental Property Template Landlord Spreadsheet Income and Expense Tracker Rental Bookkeeping Excel Google Sheets Real Estate Management

Sale Price $26.95

Original Price $38.50

-

Digital download

Real Estate Business Spreadsheet Bundle: House Flip Airbnb Calculator Bookkeeping Password Tracker Excel & Google Sheets Digital Download

$34.97

-

Digital download

WORD COUNT TRACKER | Spreadsheet for writers | Novel Word Count Spreadsheet | NaNoWriMo Tracker | Google Sheets Template

Sale Price $5.70

Original Price $11.39

-

Digital download

Excel Vacation Property Spreadsheet, Small Business Spreadsheet, Airbnb Bookkeeping, Income Expense Tracker, Rental Property Management

$29.31

-

Digital download

Rental Property Tracker Landlord Spreadsheet Multi Property Income and Expense Excel Google Sheets Rental Bookkeeping Rent Payment Tracker

Sale Price $8.86

Original Price $17.71

-

Digital download

Rental Property Tracker Landlord Spreadsheet simple Property Income and Expense Excel Google Sheets Rental Bookkeeping Rent Payment Tracker

Sale Price $5.50

Original Price $11.00

-

Digital download

Rental Property & Airbnb Management Toolkit | Excel and Google Sheets | 12 Templates

Sale Price $27.49

Original Price $109.97

-

Digital download

Rental Property Bookkeeping Google Sheets Landlord Spreadsheet Multi Property Income and Expense Tracker Excel Tenant Tracker Rent Payment

Sale Price $8.49

Original Price $16.98

-

Digital download

Rental Income and Expense Excel Tracker for Property Management Template for Real Estate Transaction Spreadsheet for Landlord Tenant Tracker

Sale Price $12.50

Original Price $25.00